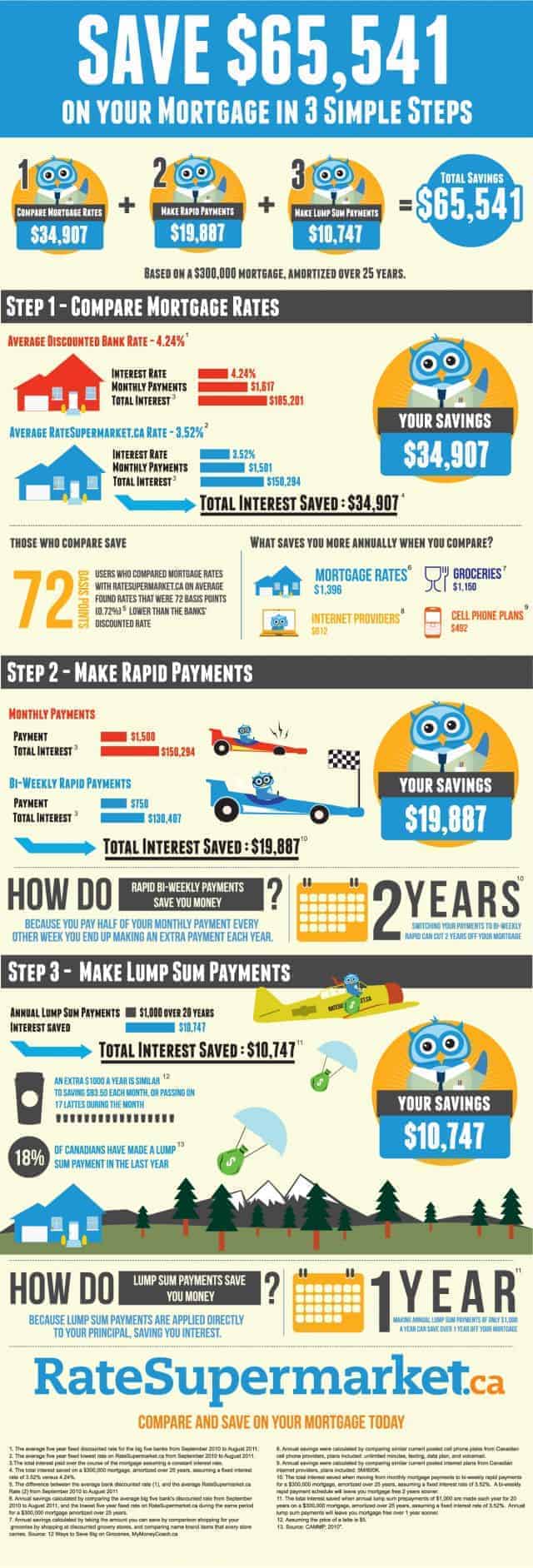

Whatever You Need To Know About House Mortgages

Authored by-Svenningsen SlaughterOwning a home is a huge responsibility which shouldn't be taken lightly. The first step is often to get approved for a mortgage, but there is a lot to learn before you dive right in. People who have taken mortgage in the past have contributed their knowledge to this article so you can learn how to avoid the mistakes they've made, so read on.

Consider the Federal Housing Authority to be your first stop when looking for a new mortgage. In most cases, a mortgage with the FHA will mean putting a lot less money down. If you opt for a conventional loan, you will be required to come up with a serious down payment, and that can mean not being able to afford the home you really want.

Predatory lenders are still in the marketplace. These lenders usually prey on home buyers with less than perfect credit. They offer low or no down payments; however, the interest rates are extremely high. Additionally, these lenders often refuse to work with the homeowner should problems arise in the future.

If your mortgage has been approved, avoid any moves that may change your credit rating. Your lender may run a second credit check before the closing and any suspicious activity may affect your interest rate. Don't close credit card accounts or take out any additional loans. Pay every bill on time.

A fixed-interest mortgage loan is almost always the best choice for new homeowners. Although most of your payments during the first few years will be heavily applied to the interest, your mortgage payment will remain the same for the life of the loan. Once you have earned equity, you may be able to refinance your loan at a lower interest rate.

Remember that your mortgage typically can't cover your entire house payment. You need to put your own money up for the down payment in most situations. Check out your local laws regarding buying a home before you get a mortgage so you don't run afoul of regulations, leaving you homeless.

If your mortgage has been approved, avoid any moves that may change your credit rating. Your lender may run a second credit check before the closing and any suspicious activity may affect your interest rate. Don't close credit card accounts or take out any additional loans. Pay every bill on time.

Get all your financial papers together before you ever see your mortgage lender. You will need to show proof of income, bank statements and all other relevant financial information. Have all the paperwork well-organized. If you are well-prepared you are more likely to be approved and the process will go quicker.

When trying to figure out how much of a mortgage payment you can afford every month, do not neglect to factor in all the other costs of owning a home. There will be homeowner's insurance to consider, as well as neighborhood association fees. If you have previously rented, you might also be new to covering landscaping and yard care, as well as maintenance costs.

Mortgage rates change frequently, so familiarize yourself with the current rates. You will also want to know what the mortgage rates have been in the recent past. If mortgage rates are rising, you may want to get a loan now rather than later. If the rates are falling, you may decide to wait another month or so before getting your loan.

Shop around for a mortgage broker that is a good fit for you. Remember that you are about to embark on a decades-long relationship with this lender, so you want to feel entirely comfortable dealing with the company. Do some online research, read reviews, look for lenders with excellent BBB ratings. Once you have sorted out a few, call and/or visit their offices. Apply with them and see if you can get a letter of pre-approval from the lender you eventually settle on.

Keep in mind that not all mortgage lending companies have the same rules for approving mortgages and don't be discouraged if you are turned down by the first one you try. Ask for an explanation of why you were denied the mortgage and fix the problem if you can. It may also be that you just need to find a different mortgage company.

Because the mortgage industry is not regulated, get your loan from a reputable company. Avoid working with a mortgage company that is only available to you online. It is important to choose a company that is known to you and who will be available to you. Do not use the services of a mortgage broker who records your income or expenses inaccurately.

Be relevant website when it comes to reporting your financials to a potential lender. Chances are the truth will come out during their vetting process anyway, so it's not worth wasting the time. And if your mortgage does go through anyway, you'll be stuck with a home you really can't afford. It's a lose/lose either way.

Shop around when looking for a mortgage. Be certain that you shop various lenders. However, also make sure that you shop around among a number of brokers too. Doing both is the only way to make sure that you are scoring your best possible deal. Aim for comparing three to five of each.

Know the real estate agency or home builder you are dealing with. It is common for builders and agencies to have their own in-house financiers. Ask the about their lenders. Find out their available loan terms. This could open a new avenue of financing up for your new home mortgage.

Take note of home buying season. Usually markets will have hot and cold selling periods. Read A lot more selling period, the more shady lenders are likely to be around. If you know what trend the market is in, you will better be able to guard against people looking to take advantage of you.

Most financial institutions require that the property taxes and insurance payments be escrowed. This means the extra amount is added onto your monthly mortgage payment and the payments are made by the institution when they are due. This is convenient, but you also give up any interest you could have collected on the money during the year.

When the bank asks a question, be honest. It is a terrible idea to lie when applying for mortgage loans. Never misstate assets or income. If you do you could find yourself saddled with more debt than you can actually afford to pay. It may seem good in the moment, but in the long-run it will haunt you.

If you have been wading through the mortgage world wondering what to do, surely now you have a better idea of the type of mortgage you need. It's up to you to pick the best situation for your largest investment. With the tips that have been provided, you should find yourself doing just that.